In contrast to what one often hears on capital streets about the dirth of natural resources that little Tunisia has to offer in the way of access to the global market, the cropping-up of press releases and studies in foreign press over the past decade or so intimate the titillation of petro-oil companies at prospects of investing in gas and oil exploration and production in the democratically-inclined ‘bright spot’ of the Arab World. The country’s «start-up democracy team» of technocrats has set the stage for economic liberalization through strategic partnerships and campaigns soliciting foreign investment. What symbolizes this shift more effectively than the development, through international concessions and collaborations, of Tunisia’s hydrocarbon industry?

New Deals – OMV Vienna and MedcoEnergi Jakarta

We have recently met with the Government of Tunisia and they have shown their strong support in welcoming us back to Tunisia to pursue oil and gas opportunites. Lukman Mahfoedz quoted in MedcoEnergi Returns to Tunisia to Expand its E&P Global Operations

Two weeks after the Austrian petro-oil company OMV confirmed its commitment—with a seal of 680 million dollars—to work with ETAP to develop Tunisia’s gas and oil exploitation operations, two press releases issued on 15 and 16 June announced a new deal signing 114 million dollars (127.7 million dollars including positive working capital) -worth of Tunisian gas and oil exploration and production sites over to the Indonesian exploration and production company MedcoEnergi.

Chinook Energy, for whom the transfer of shares represents a shift to an entirely domestic oil and gas operations, has concessions in a total of eight «prolific hydrocarbon areas» that include four exploration sites, two development sites, and two production areas: Adam, Sud Remada, Bir Ben Tartar, Jenein, and Borj El Khadra in the Ghadames Basin (on-shore), and Cosmos, Hammamet, and Yasmin in the Pelagian Basin (off-shore). As mentioned in the press release, the recent concession—retro-actively effective 1 January 2014 in spite of its pending government approval status—is not the company’s first in Tunisia; MedcoEnergi previously held production rights in the Durra and Mona gas fields and was a partner in the Anaguid concession in April 2011 allotting it 20% of a joint holdership with ETAP (30%) and OMV (50%), although MedcoEnergi subsequently sold all of its Anaguid shares (resulting in the 50-50 OMV-ETAP holdership) to OMV for 58 million dollars in November 2011.

‘Is Tunisia the New Hot Spot for Energy Investors?’

For the first time major spending has been committed to test Tunisian basins which are arguably equally prolific as those in neighbouring environments with more work performed, such as Libya. John Nelson of Africa Hydrocarbons quoted in Is Tunisia the New Hot Spot for Energy Investors?

At the time that Oil Price interviewed the CEO of Tunisia-invested Africa Hydrocarbons about «Is Tunisia the New Hot Spot for Energy Investors?», an EIA-ARI report (described below) noted that «Considerable exploration activity is underway in the Ghadames basin, with much of the activity still devoted to conventional oil and gas resources.» In 2013 Tunisia’s Ghadames and Pelagian Basins were occupied by a handful of moderately-sized (largely Canadian) oil companies, including Perenco (London), Cygam Energy (Calgary), Winstar Resources (Calgary), Chinook Energy (Calgary), and Africa Hydrocarbons (Calgary), in addition to some of the bigger names such as OMV (Vienna) and Shell Oil (The Hague).

We have heard that Shell and others have an interest in testing shale1 (also called “unconventional”2) plays3 within the region. The possibility for an unconventional play type also exists on our acreage but we have chosen what we believe is the “low hanging fruit” [conventional4] to target first. John Nelson of Africa Hydrocarbons quoted in Is Tunisia the New Hot Spot for Energy Investors?

A US Energy Report on Tunisia’s Shale Gas and Oil Prospects

US Energy Information Administration commissioned this ‘cutting edge’ shale gas and shale oil resource assessment, to incorporate the new exploration and resource information that will become more valuable during the coming years, helping keep this World Shale Resource Assessment ‘evergreen.’ EIA-ARI, World Shale Gas and Shale Oil Resource Assessment

In June 2013, the US Energy Information Administration (EIA) published the World Shale Gas and Shale Oil Resource Assessment assessesing 137 shale formations in 41 countries outside of the United States. The study, prepared by Advanced Resources International (ARI), is long and technical though not incomprehensible with a bit of vocabulary clarification, and gives some indication of how Tunisia falls within a vision (of powerful players in the energy industry) for the future of hydrocarbons.

It is clearly important for those interested in the evolution of global markets for liquid fuels to assess the magnitude and extent of recoverable resources from shale formations.EIA-ARI, pp 13, Technically Recoverable Shale Oil and Shale Gas Resources

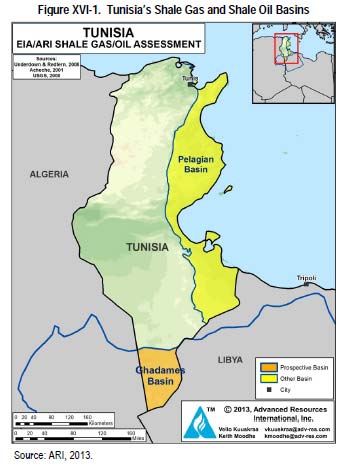

Ten of the report’s 730 pages are dedicated to the aforementioned ‘possibility for unconventional play’ in Tunisia’s Ghadames Basin in the south and, to a lesser extent, the Pelagian Basin covering both on- and off-shore resources in the east. According to the report’s ARI authors, the Ghadames (also called Berkine) Basin spans eastern Algeria, western Libya, and southern Tunisia. Its two shale fomations constitute 114 trillion cubic feet (Tcf) of risked5 [as opposed to unrisked6] shale gas in-place7 of which 23 Tcf is risked, technically recoverable8 shale gas resource, as well as 29 billion barrels of risked shale oil in-place, 1.5 billion barrels of which is classified as risked, technically-recoverable shale oil resource.

The Silurian-age Tannezuft ‘hot shale’9 characteristic of the Ghadames basin is a prevalent rock source for conventional gas fields throughout the MENA region; the Ghadames formation is an organic-rich marine shale whose thermal maturity10 ranges from early/ immature (wet gas11 and condensate12) to late/postmature (dry gas13) north to south respectively. It constitutes 43 Bcf (bioconcentration factor as a measure of resource concentration)/mi2 of wet gas and 3.1 million barrels/mi2 of condensate. The risked ressource in-place is 45 Tcf of shale gas and 0.8 billion barrels of shale oil and risked, technically recoverable resources of 11 Tcf of shale gas and less than 0.1 billion barrels of shale oil.

The Upper Devonian Frasnian Shale, whose thermal maturity also ranges from early/immature (wet gas and condensate) to late/postmature (dry gas) north to south respectively, constitutes 80 Bcf/mi2 of wet gas, 7 million barrels of condensate, 31 million barrels/mi2 of oil, and 101 Bcf/mi2 of dry gas. Its risked resource in-place is 69 Tcf of shale gas and 28.5 billion barrels of shale oil.

Two hydrocarbon systems constitute the Pelagian Basin. The Jurassic-Cretaceous Petroleum System contains Jurassic Nara, Early Cretaceous (Albian) Fahdene, and Late Cretaceous Bahloul Formations with a thermal maturity range from early mature to late mature, while the Tertiary Petroleum System contains the Early Eocene Bou Dabbous Formation with a thermal maturity ranging from early mature to mature.

A Glimpse into the Hydrocarbon Industry

We benefitted greatly from the major new efforts on assessing and pursuing shale gas and shale oil resource, stimulated in part by the 2011 ETA/ARI study in countries such as Algeria, Argentina and Mexico, among many others.EIA-ARI, Technically Recoverable Shale Oil and Shale Gas Resources

If the US EIA has benefitted from research and assessments of international shale gas and oil development prospects, the information presented is equally pertinent to energy-affiliated institutions and the citizenry of any country whose unconventional gas plays potential is a feature of the report, which also offers a glimpse into how the US sets about selecting investments abroad. In Tunisia, in light of repetitious references in international media to the country as a political «bright spot» and «technological hub» of the MENA region, a «hot spot» of the hydrocarbon industry, in light of foreign interest to invest in the interim government’s «start-up democracy,» in light of the press releases and extensive studies published by foreign institutions that discuss concrete and/or potential plans for the reform and development of Tunisia’s economic, political, technological landscapes, Tunisian citizens especially deserve access to the content of such studies and agreements as they do, after all, concern among other things the operation of state institutions and management of natural resources.

1 shale – fine-grained sedimentary rock that can be rich resources of petroleum and natural gas

2 unconventional oil – consists of a wider variety of liquid sources including oil sands, extra heavy oil, gas to liquids and other liquids

3 (gas or oil) play – a group of oil fields or prospects in the same region that are controlled by the same set of geological circumstances

4 conventional oil – a category of that includes crude oil and natural gas liquids and condensate liquids, which are extracted from natural gas production. In general conventional oil is easier and cheaper to produce than unconventional oil.

5 risked reserves – either probable or possible reserves depending upon the amount of uncertainty involved and basically represent poorly developed or undeveloped oil

6 unrisked reserves – those which have already been developed by drilling and production and thus have a very reasonable certainty of being produced

7 gas in place (GIP) – the total volume of natural gas in an underground rock-formation

8 technically recoverable resources (TRR) – represent the volumes of oil and natural gas that could be produced with current technology, regardless of oil and natural gas prices and production costs. pp 10

9 hot shale – shale of particularly high uranium content

10 thermal maturity – a measure of the degree to which organic metamorphism has progressed, and gives a crude indication of the maximum temperature the rock has experienced. Three levels of maturity are recognized by petroleum geochemists, early/immature (methane), peak/mature (oil), and late/postmature (gas) (definition adapted).

11 wet gas – natural gas that contains less methane (typically less than 85% methane) and more ethane and other more complex hydrocarbons.

12 condensate – a low-density mixture of hydrocarbon liquids that are present as gaseous components in the raw natural gas produced from many natural gas fields

13 dry gas – natural gas that occurs in the absence of condensate or liquid hydrocarbons, or gas that has had condensable hydrocarbons removed

This search is powered By Nawaat experimental generative artificial intelligence. Begin typing your search or question above then press return. Press Esc to cancel.

This search is powered By Nawaat experimental generative artificial intelligence. Begin typing your search or question above then press return. Press Esc to cancel.

Interesting article Vanessa

Tunisia sure looks like a success compared to other “Arab Spring” nations, but regarding the newly adopted Tunisian Constitution, all issues relating to natural resources contracts must be approved by the National Constituent Assembly. Apparently, the relevant government departments are still developing procedures for implementing this new protocol. This has resulted in numerous delays on oil and gas exploration projects in Tunisia right now. Do you, by any chance, know of this issue and how soon it can be resolved? some companies may halt investments as the wait drags on indefinitely, which is not good fo the country.

Well who cares, Tunisia is not getting any benefits from oil and gas, in fact almost all of the natural resources, they’re being taken almost for free, and some actually ARE indeed taken for free.

The economy already doesn’t rely on oil, it’s like if we don’t have any, it’s a big file full of corruption, they lie about how much oil Tunisia really produce (caught many times, saying wrong numbers while the oil companies saying other numbers), there are 64 oil companies working in Tunisia (what are they doing if there is no oil…), and they never report the discovery of the new oil and gas resources in the national news, goverments try to keep a blind eye about it and NEVER talk about it, despite Tunisia having huge amounts of oil and gas, mostly discovered after the revolution, enough to pay all our debts and boom the economy.

It is really hopeless…

j ai assisté a une conférence organisée par la Fondation Temimi sur la ” corruption dans le domaine du pétrole” Samedi 14 juin , il y avait trois intervenants ,le premier qui était présenté comme un ‘expert international dans le domaine ‘ et qui a acquis ce titre a travers ses sorties dans les medias car en fait c est un monsieur qui n a même pas parait il le bac , et qui prétend l expertise alors que Personne dans le domaine en Tunisie ne le connait. ce Monsieur impressionna l assistance chauffée a blanc par le mot magique ‘ Corruption ‘ . il a avoué qu’ il était en fait un broker ‘samsar’ et qu’ il a introduit une petite compagnie Ukrainienne qui a eu le Permis de recherche Araifa . on a entendu tellement d imbécilités pour quelqu un qui connait un peu le domaine tel que par exemple ; il peut acheter n importe quel ingénieur de l ETAP pour 200 Dinars ou un diner!!!! ,que tel directeur qu’ il a nommé a vendu des données de l ETAP pour 700 000 DT a Qatari invest ? il faudrait introduire le nom du Qatar pour que l histoire soit crédible !!!! sachant que le Qatar ne s’est jamais intéressé a l exploration pétrolière en Tunisie? le potentiel petrolier de la Tunisie est bien modeste pour le Qatar!!!!!! il affirmait aussi que sa société Ukrainienne( qui est un petite société qui n a rien dans le ventre et ce d apres les ingénieurs ETAP) avait une technologie qui pouvait nous trouver du pétrole avec des images satellites ! ce qui est du ridicule.!!!!!! il a affirmait qu il représentait une compagnie qui vendait des appareilsi sont extraordinaires .et peuvent nous sauver … .. il a aussi mis en cause un professeur en géologie de la FST et l ETAP dans la gestion d une formation d un an en géosciences ( une histoire monté il parait par Jalousie par un autre Pr qui n a pas enseigné dans la formation). l assistance était émerveillé ,il y avait même des députes et personne n a réagi quand ce monsieur a commencé a accuser des Personnes ! la fondation Temimi était tombé très bas . ca sentait le vinaigre et je pense que ce Monsieur était manipulé par des personnes cherchant a discréditer le personnel de l ETAP en entier et certains personnes cités par ce Monsieur. il répétait en fait des choses qu’ il ne maitrisait pas comme sismique 2D , 3D , géologie géophysique il saute du Coq a l Ane…. une Personne présente a demandé au Pr Temimi si il avait consulté le CV de ce Monsieur avant de l inviter, la réponse est non ! et c’est malheureux pour la réputation de la Fondation Temimi , inviter un Samsar et le présenter a l audience comme un expert et un même un Docteur. Incroyable Pr Temimi comment vous êtes tombé dans un tel piège , vous avez évoqué la liberté d’expression bien sûr , Mais ou est la crédibilité quand on présente un bac moins comme un expert et même un Docteur.

on a ensuite eu une conférence d une avocate qui se prend pour un ‘Che Guevara’ elle a affirmé en autres que les ambassades des USA et de la GB ne lui ont pas livré un visa pour assister a un séminaire sur les Contrats pétrolières , ‘théorie du complot’ car peut être elle était trop ‘ militante’ elle a été sauvé par le brésil ou elle s est déplacé pour assister a ce séminaire organisé par la boite Petro……..après ce séminaire elle est devenue experte dans les contrats alors qu’ il faudrait des dizaines de séminaire pour comprendre les ABC du domaine!!! cette personne ne connait pas la différence entre un Permis et une Concession et accusé a tort a travers de corruption , l audience était émerveillé par de tel idioties . elle répétait les remarques de la cour des comptes sans bien sur dire un mot sur les réponses des responsables du Secteur sur ces remarques!!!!! et affirmait même que notre potentiel pétrolier est grand !!!! a t elle appris ca dans le dit seminaire ! elle connait maintenant le secret de notre sous-sol !!!!!! il fallait taper ,taper sur les sociétés du secteur et les faire partir coute que coute pour faire entrer des petites compagnies comme celle que notre expert samsar a fait enter et qui découvriront du pétrole avec des images par satellites !!!!!!!!!. Il ya des rumeurs que j espère qu’ il ne sont pas vrais qui disent que des personnes ont demandés des sommes importantes a des compagnies pétrolières sinon ils auront affaire a une compagne de diffamation ??? de Nouveaux Trabelssia en vue après la révolution

un autre intervenant qui était a la tète d une compagnie pétrolière qui a perdu un permis de recherche en Tunisie car la demande d extension du Permis était conditionné par ‘ l accord du conseil d administration de sa société’ .ce qui est inacceptable et ridicule . ce Monsieur qui conseille des députés a l assemblée a affirme que les extensions en Temps des Permis était illégales !!! alors que sa société a bénéficié d extension et même d un 4 eme renouvellement du Permis, alors qu’ il était a la tète de la société !!!! bizarre alors que les extensions de Permis sont légales et codifies dans le Code. avant l apparition du Code les extensions au delà de deux ans sont sujet a un avenant a la convention et approuvés par loi . Bien sûr l extension doit être conditionné par la réalisation de travaux supplémentaires ou montrer qu’ il ya des raisons valables qui ont empêchés la réalisation des travaux a temps ( absence d appareil de forage en Tunisie, de sociétés de services surtout pour l acquisition sismique, problèmes fonciers et après la révolution les problèmes sociaux….) et ce qui est étonnant est qu’ on pousse l ANC par une compagne a travers les medias a ne pas donner des extensions a des compagnies pétrolières qui ont investit en Tunisie meme apres la révolution , alors que tous les projets d infrastructures dans le pays sont en retard ,on veut en fait les faire partir pour faire entrer d autres moyennant commissions et bakchich !!!!!! j invite la fondation Temimi a le devoir de donner une copie de l’enregistrement de la Conférence a l ETAP ,et aux personnes dont les noms ont été cités et la Justice doit faire son travail car je pense qu’ il y a beaucoup de diffamations et de mensonges dans cette conférence et la justice doit arrêter cette mascarade.

L ANC doit faire attention a la crédibilité de la Tunisie et encourager les sociétés pétrolières sérieuses a investir plus , depuis deux ans il n y a eu qu une petite découverte de pétrole malgré le forages de l ordre de vingt puits de recherche ; la recherche pétrolière est une activité tres risqué ( probabilite de decouverte 10 % en moyenne ) ,tres gourmande en capital (des millions de dollars investis dans la plupart des cas a fonds perdus) et les résultats sont a long terme (7 a 10 ans depuis le debut des operations de recherches), la stabilité politique et des engagements pris par l ETAT sont très importantes ; Sinon on risque des procès en arbitrage international qui peuvent couter très cher a la Tunisie plus de 200 millions de dollars pour un seul cas . L ANC doit être prudente et être bien conseillée par de vrais experts par des gens qui essayent de se venger, il faut faire attention le pays risque gros ; en 2014 aucun puits de recherche n a été foré et la production pétrolière baisse de 12% par an alors que notre consommation augmente de 10% au minimum ? le budget de l ETAT est gangrené par les importations de gaz et de produits pétroliers payés très cher en devises et qui sont subventionnés . il y a aujourd hui 36 permis libres et aucun investisseur ne s est intéressé!!!!!!! nos invitons nos chers hommes d affaires d investir dans le domaine .” its high Risk high Reward”

Interessant Mohamed

Pensez vous que les autorites utilisent la nouvelle constitution comme excuse pour reclamer plus de commissions des companies explorant en Tunisie?

@aristide

c est des ”samsar” en collaboration avec des avocats et meme des journaux electroniques , c est les rumeurs qu on entend tous les jours. les Autorites n ont rien a voir la dedans, il doivent faire une enquete sur ces rumeurs pour arreter cette mafia

@aristide

c est des ”samsar” en collaboration avec des avocats et meme des journaux electroniques , c est les rumeurs qu on entend tous les jours. les Autorites n ont rien a voir la dedans, ils doivent faire une enquete sur ces rumeurs pour arreter cette mafia

@aristide

c est des ”samsar” en collaboration avec des avocats et meme des journaux electroniques , c est les rumeurs qu on entend tous les jours. les Autorites n ont rien a voir la dedans, ils doivent faire une enquete sur ces rumeurs pour arreter cette mafia

Je suis d’accord que les rumeurs causent pas mal de problemes

Mais j’ai appris que certaines companies ont des projets retardes par le processus que la nouvelle constitution a mise en place. J’esperes que cela ne va chasser des investisseurs interesses. Ce serait dommage pour la Tunisie.

We have to be very careful of what it is stated until discovery is made and well is tested. In other words (mainly in O&G industry) we have we distinct between business talk, opportunities and reality on the ground.

I have been for 24 years in drilling and production business and it is very difficult to deal with geology and O&G production as an exact science. Good investment are good to needy Tunisia, but it is better to make an investment with good and long socioeconomic return. Example why don’t we drill for deep thermal wells for water desalination and power generation? Isn’t a long term investment with great economic, financial and social benefits return?

Unconventional development in Tunisia is possible but its still too expensive, the cost of drilling and fracking a well is very expensive compared to US where competition high and a lot of services companies compete in the market. the need of large quantities of water to frack a well (20.000 to 30.000 M3 per well ) is another problem and only salty water shall be used from sea or others geological formation that contains salty water not useful to Agriculture . Unconventionel is an industry ,a lot of wells shall be drilled (hundreds) to sustain an economic production because an unconventional well production well decline about 40 % the first year I think this type of exploration will be developed economically in Tunisia only if unconventional succeed in Algeria so there will be a big market for service companies in North Africa .at this stage Tunisia will not benefit too much from unconventionnal because the cost is High an the tax revenues to the state will limited . ETAP will also have to invest a lot of capital in the development phase when it participate at 50%. the most appropriate type of contract for unconventional is the Production sharing contract where ETAP does not bear any expenses in development and production phase. So cost optimization and cost control and use of salty water is the Key of success of unconventional business in Tunisia.

we need unconventional oil or gas to limit imports and secure our energy needs from the country .To be dependent of import of gas from Algeria is risky ( 60% of our needs ) and very expensive (paid cash and in dollars) .

solar energy and wind energy shall be encouraged , private sector can do miracles and i call STEG syndicates to stop their campaign against private power generation from renewable s , the country will benefit from less import of gas and ave n a lot of hard currency . we need to follow the exemple of Germany ,we can do it , every house shall have solar panels to produce its power needs !!!! we need to partner with Chinese companies to develop an industry of solar panels in Tunisia; Why not ? train young people on how to install and maintain solar power. We can trough insure 30 % to 40% of our energy needs from solar and wind.

Menace Contre Zerguine ? qui a interet

je vais donner un apercu sur ce dossier . une extension d un permis de recherche ou l investisseur investit a son risque en faisant des activites de sismique et fore des puits d exploration sil ne trouve rien 90% des cas ,il perd ses investissements . s il trouve une decouverte commerciale il a le droit de développer la decouverte . l ETAP qui na pas depenses aucun millimesdans la recherche du petrole et a droit de participer a 50% dans le developement de la decouverte. Bien sur en cas de production L investiseur et ETAP paie une redevance ( part de la production delivré a L ETAT gratuitement ) et paie un impot sur benefice a un taux elevé de 50% . La Tunisie a une part de la Rente petroliere ( benefice) de chaque champ de l ordre de 80%. l extension en Temps d un permis

de recherche est permis par la loi il est conditionné par soit l engagement de travaux supplementaire par rapport a ses engagements initiaux soit il faut que l investisseur montre qu il a eté empeché de faire ses travaux ( problemes sociaux; absence d appareil de forages disponibles en Tunisie…) l extension est accordé par le comité consultative de l energie ( CCH) et accorde par arreté du ministre(voir le code Des Hydrocarbures) . Pour les Permis qui sont octroyés avant la promulgation du Code . il ya des extention qui sont accordés par des avenants a la Convention Ces avenants negociés entre l investisseur , LETAP et le Ministere de l industrie . Moyennant l extension du Permis de 2ans la societe petroliere s engage a investir en forant des puits de recherches de petroliere et en effectuant d autre travaux de recherches . ces avenants doivent etre approuvé par le parlement et promulgues par Loi. apres avoir conclus des avenants les compagnies petrolieres en bonne foi ont commencé les travaucx de recherches et investit des milliards ,car ils ont negocies ces avanants par le ministre qui represente l ETAT. le comité de l energie a nié au ministre en charge des Hydrocarbures ses rerogatives en se basant sur l article 13 de la Constitution.biensur il ya eu l intervention d avocats samsar et autres pseudo experts qui faisait du lobying pour empecher le comite de voter ces avenants pour recuperer les permis et faire entrer des petites compagnies et profiter des investissements deja realisés par les investisseurs moyennant bien sur des commissions Juteux. beaucoup de personnes ont alerté le comité d energie mais ce comité n a jamais accepté d inviter des experts petroliers reconnus dans le domaine. les Samsar ont des petites companis sous la main et qui attendent .le Comité oublie ou n est pas conscient que les investisseurs peuvent intenter des procés en Arbitrage international a l encontre de l ETAT Tunisien car il ont investit des milliards en bonne foi et ont un avenant signé par le représentant de l ETAT, ce qui va geler les Permis pendant des années en attendant la décision de l arbitrage!!!!!.

les societés perolieres ne menancent personnes ils sont cotes en Bourse , ils ont leur réputation a préserver , cette histoire a ete monté par les Samsar qui veulent creer une histoire pour salir les investisseurs qui respectent les lois du pays. les faire partir pour faire entrer des compagnies qui n ont ni expertise ni assez de fonds a risquer Monsieur Zerguine ne tombe pas dans le piege ?